If you’re running a business, you’re generally more susceptible to tax penalties than when you’re earning solely as an individual taxpayer. In the Philippines, these BIR penalties are charges imposed for violations of tax laws. While some may seem minor, they can quickly add up once surcharges and interest are applied, creating a heavier financial burden than expected.

In such cases, formally requesting a penalty reduction can help ease your financial load while demonstrating your good faith and intent to comply with your tax obligations. This process isn’t always familiar to new or small business owners, but it can make a big difference when handled properly.

In this third and final installment of our BIR Letters and Notices blog series, you’ll learn how to reduce your BIR penalties—understanding their legal basis, applicable rates, and how to write an effective request letter to the BIR.

BIR Penalties: When and How They Apply

The Bureau of Internal Revenue (BIR), being the tax authority, assesses and collects national internal revenue taxes and enforces penalties for violations of the National Internal Revenue Code (NIRC) and other regulations. These violations include late filing or payment of tax returns, underdeclaration of income, failure to register or update information, and noncompliance with invoicing or documentation requirements.

For instance, BIR penalties for late filing of tax returns with tax due include a 25% surcharge on the tax due and an additional penalty of 12% interest per year or 1% per month. Upon conviction, you may also be punished by a fine of not less than PHP 10,000 and imprisonment of not less than 1 year but not more than 10 years.

On the other hand, if you fail to file an information return or keep any record required by the Tax Code or by the BIR commissioner, you may be demanded to pay a penalty of PHP 1,000 for each failure, provided that the aggregate amount for all during a calendar year does not exceed PHP 25,000.

Understanding BIR Compromise Penalties and Abatements

A compromise penalty is a reduced sum that the Bureau of Internal Revenue (BIR) may collect from you as a taxpayer to settle criminal liability for violations of the National Internal Revenue Code (NIRC) subject to BIR evaluation and applicable laws.

Under Section 204 of the NIRC, as implemented by Revenue Regulation (RR) 30-2022, the BIR Commissioner may allow you to compromise the payment of any internal revenue tax when (a) there is reasonable doubt as to the validity of the BIR’s claim against you, or (b) your financial records clearly show that you are unable to pay the assessed tax. All criminal violations may be compromised except those already filed in court or those involving fraud.

Furthermore, as explained in BIR Regulations 30-2002, doubtful validity applies when an assessment is questionable due to jeopardy, arbitrariness, presumption, lack of protest or reinvestigation, deficient demand notice, reliance on the best evidence rule, or doubtful authenticity of a waiver of the statute of limitations.

In these cases, the minimum compromise rate for doubtful validity is 40% of the basic assessed tax. However, you may request a lower rate by submitting a written explanation supported by legal or factual grounds, subject to approval by the National Evaluation Board (NEB).

Meanwhile, a compromise penalty for financial incapacity may be granted if your corporation has ceased or dissolved, has at least 50% capital impairment, or shows a net worth deficit with insufficient liquid assets to pay its tax liabilities. As an individual taxpayer, you may be granted if you have no leviable property aside from a family home, earn below specific thresholds with no other leviable assets, or are declared bankrupt or insolvent.

Consequently, BIR compromise rates depend on your circumstances: low- or no-income individuals and those with zero or negative net worth pay 10%; dissolved or recently non-operating corporations pay 20%; severe capital impairment pays 40%; and bankrupt or insolvent taxpayers pay 20%, with rates applied based on the specific condition.

Additionally, the BIR Commissioner may also abate or cancel a tax liability, when (a) the tax or any portion thereof appears to be unjustly or excessively assessed or (b) the administration and collection costs involved do not justify the collection of the amount due (Section 24, NIRC).

Types of Request Letters for BIR Penalty Relief

When dealing with tax compliance issues, you may need to submit specific letters to the BIR to address penalties, open cases, or payment difficulties.

Letter of Cancellation of Open Case

You need to write this letter if the BIR’s system still shows an open case even after you have submitted the required tax returns. In this letter, you formally request the BIR to cancel the open case entry reflected in their records.

Request Letter for Waiver or Reduction of Penalty/Surcharge

You use this letter to explain the reason for your delay or error in tax compliance and to request relief from penalties or surcharges. After you submit this letter, the BIR evaluates your explanation and decides whether to grant full relief, partial relief, or deny the request, based on the applicable legal provisions.

Request Letter for Payment Arrangement/ Installment Plan

You send this letter to the BIR when you are unable to settle your full tax liability in one payment. In the letter, you ask for approval to pay through installments, explain your financial difficulty, and propose a payment schedule that you can reasonably follow.

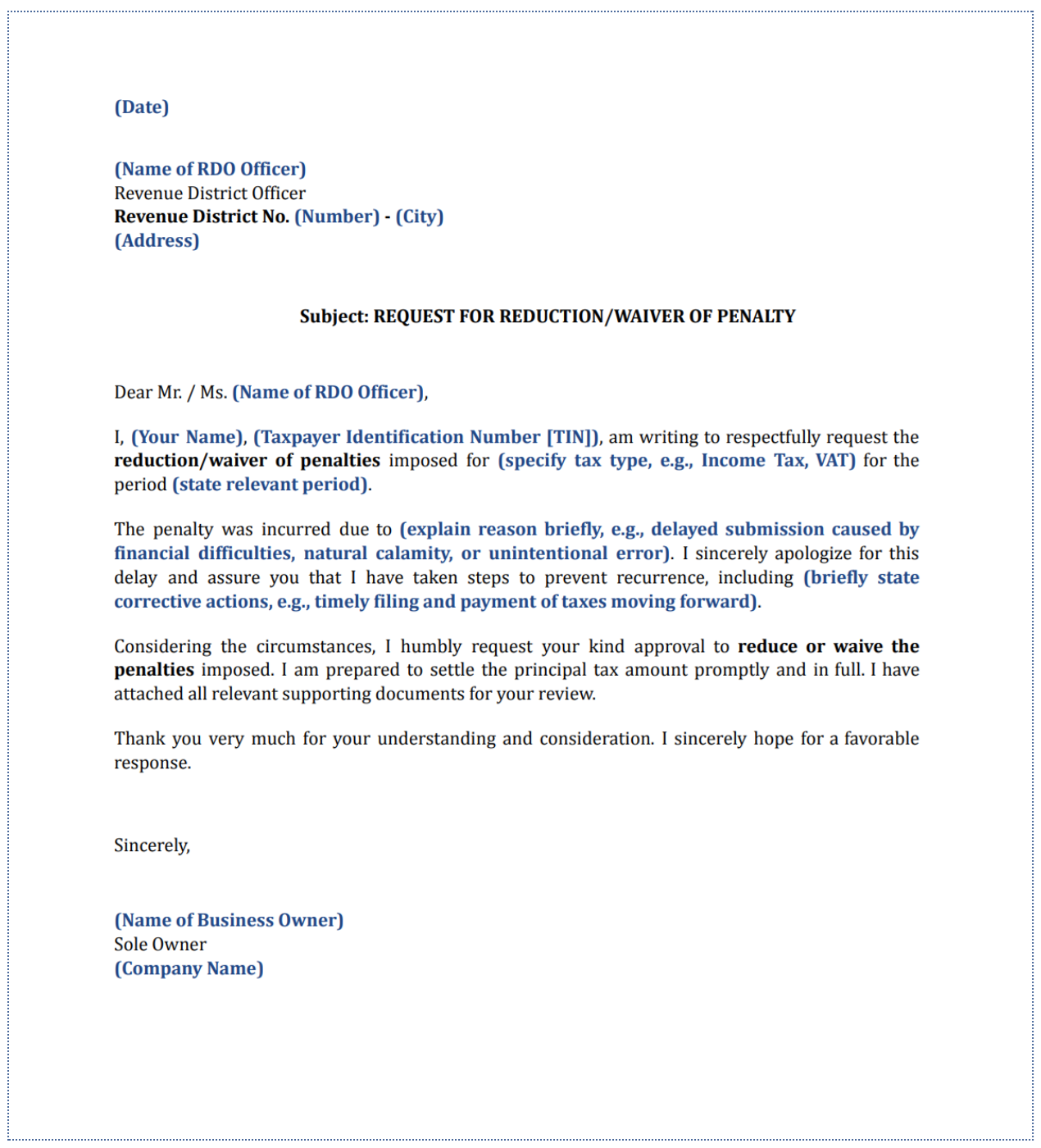

Sample Request Letter for Reduction/Waiver of BIR Penalties

When drafting the request letter, take note of the following guidelines and best practices that can help you ensure the message is clear, professional, and effective:

(1) Use a formal and professional tone. Address the BIR officer appropriately and respectfully. Avoid casual language and maintain a polite, businesslike tone throughout.

(2) Include essential identification details. Provide your full name or company name, Taxpayer Identification Number (TIN), and contact information. Clearly indicate the relevant tax type, tax period, and other information.

(3) Clearly state the purpose of your letter. State upfront that you are requesting a reduction or waiver of the BIR penalties. Specify the exact penalties or surcharge you are addressing.

(4) Provide a valid and honest explanation. Explain the reason for the delay or non-compliance, such as financial difficulties, illness, natural calamity, or administrative error. Be concise, but include enough detail to show the legitimacy of your request.

(5) Demonstrate good faith and corrective actions. Show that you have complied with your tax obligations as much as possible. Mention the steps you have taken to prevent future delays or errors, such as updating accounting processes or ensuring timely filing moving forward.