Responding promptly and properly to BIR letters and notices is crucial for every taxpayer. Your timely and accurate responses not only prevent unnecessary penalties, audits, and legal complications but also demonstrate good faith and compliance with the Philippine tax regulations.

In the first part of our series, we explored the different types of letters and notices issued by the Bureau of Internal Revenue (BIR) to taxpayers. In this follow-up article, we focus on practical strategies for responding to these communications and share best practices to help you handle tax matters with confidence.

Common Taxpayer Response Letters to BIR Letters and Notices

The table below breaks down the most common taxpayer response letters to BIR notices, along with their purposes, descriptions, and the scenarios where they apply.

Response Letter | Purpose | Application | |

1 | Letter of Compliance/ Response to Open Case Notice | To inform the BIR that you have already filed or complied with the tax return or requirements indicated in the notice | Upon receipt of the BIR “Open Case Notice” or “Non-Filing Notice” |

2 | Letter Explaining Non-Filing | To explain why a particular tax return or attachment was not filed within the deadline | When your business is non-operational, closed, or had no transaction |

3 | Letter for Cancellation of an Open Case | To formally request the BIR for the cancellation of an open case entry | When the BIR’s system still shows an open case after submission of tax return or compliance |

4 | Request for Waiver or Reduction of Penalty/ Surcharge | To request reconsideration of penalties due to late or erroneous filing | After receiving a penalty notice |

5 | Letter of Presentation/ Compliance with Letter of Authority (LOA) | To acknowledge receipt of the LOA and confirm willingness to comply | Upon receipt of the Letter of Authority (LOA) |

6 | Request for Extension to Submit Documents | To request additional time gather and submit BIR-requested records | During BIR audit, especially if deadline is near |

7 | Letter of Non-Availability of Records | To explain to the BIR the missing or lost financial records | When financial records are lost or destroyed (e.g., due to fire, system crash, etc.) |

8 | Letter of Explanation | To provide explanation on discrepancies noted by the BIR | During audit discussions or upon examiner’s request |

9 | Request for Assessment Based on Best Evidence Available (BEA) | To ask the BIR to assess using available information if records are unavailable | For small or inactive taxpayers or those without complete books |

10 | Compliance Letter for Subpoena Duces Tecum (SDT) | To submit required documents as per subpoena | Upon receipt of Subpoena Duces Tecum (SDT) |

11 | Request for Clarification or Extension (SDT) | To seek clarification or more time to comply with the subpoena | Before the Subpoena Duces Tecum (SDT) deadline |

12 | Letter Explaining Non-Compliance (SDT) | To justify to the BIR why requested documents cannot be produced | If documents are lost or unavailable |

13 | Reconciliation/ Explanation Letter (NOD) | To explain or reconcile figures questioned in the Notice of Discrepancy (NOD) | After receipt of the Notice of Discrepancy (NOD) |

14 | Position Paper | To present formal arguments against the BIR findings | After Notice of Discrepancy (NOD) or Preliminary Assessment Notice (PAN), during protest phase |

15 | Reply to Preliminary Assessment Notice (PAN) | To respond to PAN and contest BIR findings | Within 15 days from receipt of the Preliminary Assessment Notice (PAN) |

16 | Protest Letter for Final Assessment Notice (FAN) | To formally dispute the BIR assessment | Within 30 days from receipt of the Final Assessment Notice (FAN) |

17 | Request for Reconsideration/ Reinvestigation | To seek review of BIR findings or reassessment | After receipt of the Final Assessment Notice 9FAN), depending on the taxpayer’s position |

18 | Request for Payment Arrangement/ Installment Plan | To propose a staggered payment scheme | When the taxpayer cannot pay the full liability |

19 | Request for Lifting of Warrant of Garnishment (WOG) | To seek lifting of bank garnishment or levy | After enforcement of collection |

20 | Letter Explaining Already Paid/ Offset Taxes | To clarify that taxes assessed were already settled or offset | Upon receipt of a collection notice |

21 | Request for Revalidation/ Extension of Letter of Authority (LOA) | To ask the BIR to revalidate the expired Letter of Authority (LOA) | If the audit continues beyond the validity of the Letter of Authority (LOA) |

22 | Request for Cancellation/ Lifting of Assessment | To request cancellation of erroneous or duplicate assessment | After receiving multiple assessments |

23 | Request for Closure/ Termination of Business | To request for a BIR clearance and business closure | For inactive or closed businesses |

24 | Letter for Withdrawal/ Amendment of Returns | To request permission to amend or withdraw filed tax returns | When correcting filed return errors |

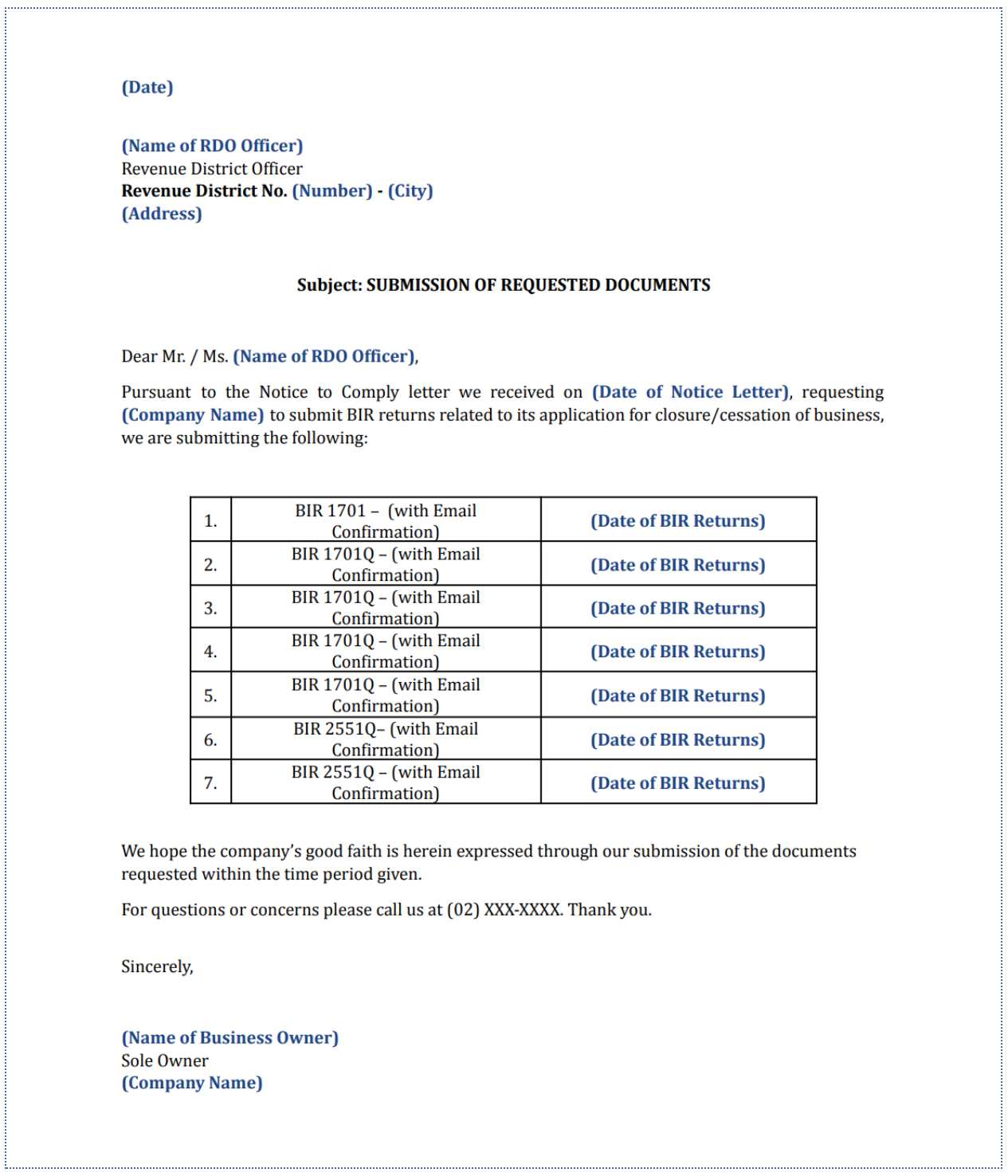

Sample Letter of Compliance or Response to Open Case Notice

As mentioned, a Letter of Compliance or Response to Open Case Notice serves as a formal response to the BIR Open Case Notice or Non-Filing Notice, providing proof of document submission and demonstrating the intent to resolve any open or pending case. Here are some key guidelines and best practices when drafting the letter:

(1) The date in the dateline indicates when you wrote the letter and serves as proof that you complied within the required period (or as indicated by the BIR receiving stamp).

(2) The inside address specifies the correct BIR Revenue District Office (RDO) and the name of the officer and ensures that your letter is properly addressed and delivered.

(3) The subject line summarizes the purpose of your letter, e.g., submitting the requested documents in response to an Open Case or Non-Filing Notice.

(4) Your salutation should respectfully address the Revenue District Officer using “Dear Mr./Ms.” followed by the last name.

(5) In the opening paragraph, you should acknowledge receipt of the notice and state your intent to submit the required documents.

(6) In the body of the letter, you should list all the BIR forms being submitted, including the dates filed and email confirmations, to serve as proof of compliance. Presenting these documents in a clear table or numbered list is important to make the submission organized, easy to review, and efficient for verification by the BIR.

(7) The closing paragraph should express your company’s good faith, confirm that the submission was made within the prescribed period, and provide contact details for follow-up.

(8) Finally, your signature block should include your name, title, and company, making the letter official and verifiable.